Student Loan Debt and Bankruptcy: What You Need to Know

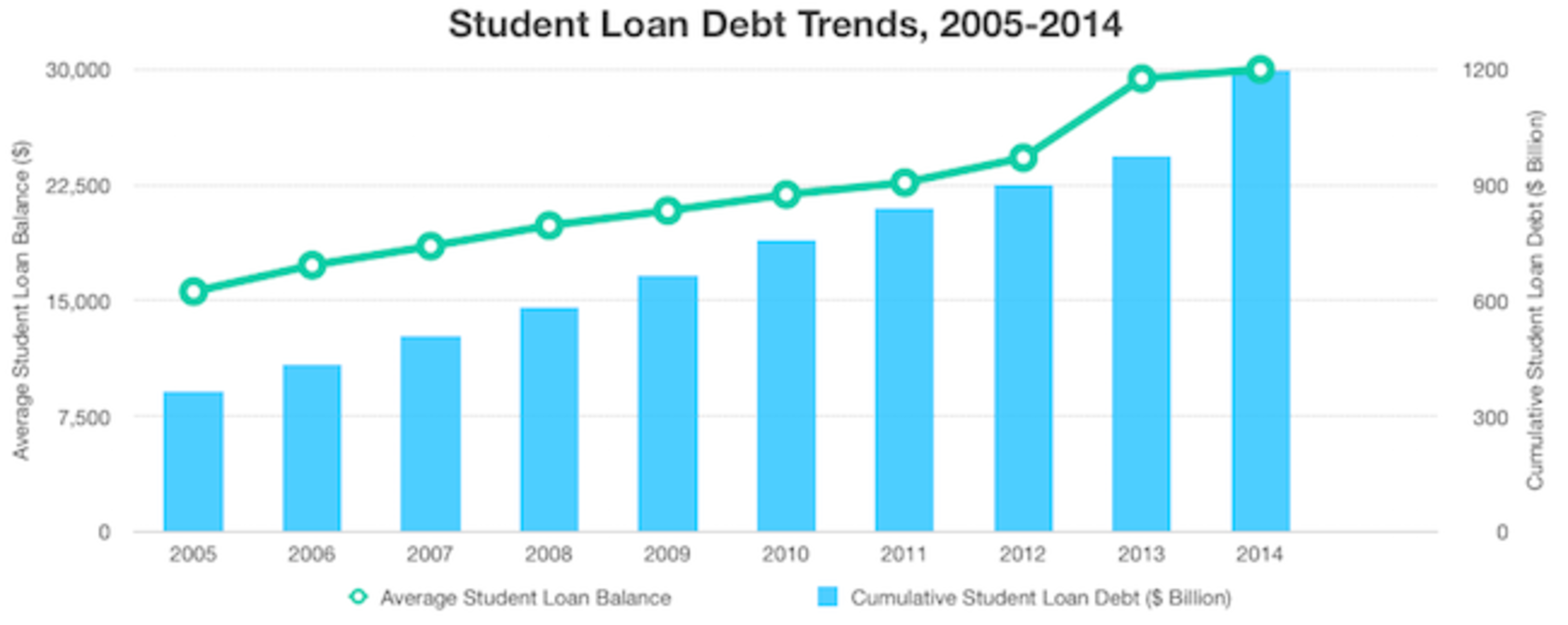

Students in the United States owe more than $1 trillion in student loans. A 2014 college graduate is looking at an average of $33,000 in student loan debt, an increase of more than 40% since 2008.1,2 And this is before considering debt from credit cards, auto loans, and mortgages. Students are entering the workforce with more debt than ever before, and the trend is only getting worse.

Data Source: Federal Reserve of New York

A college degree is more important than ever to enter high-earning professions, yet the cost of college discourages many students from trying to further their education. Those that do choose higher education feel the burden of loan debt for years to come.

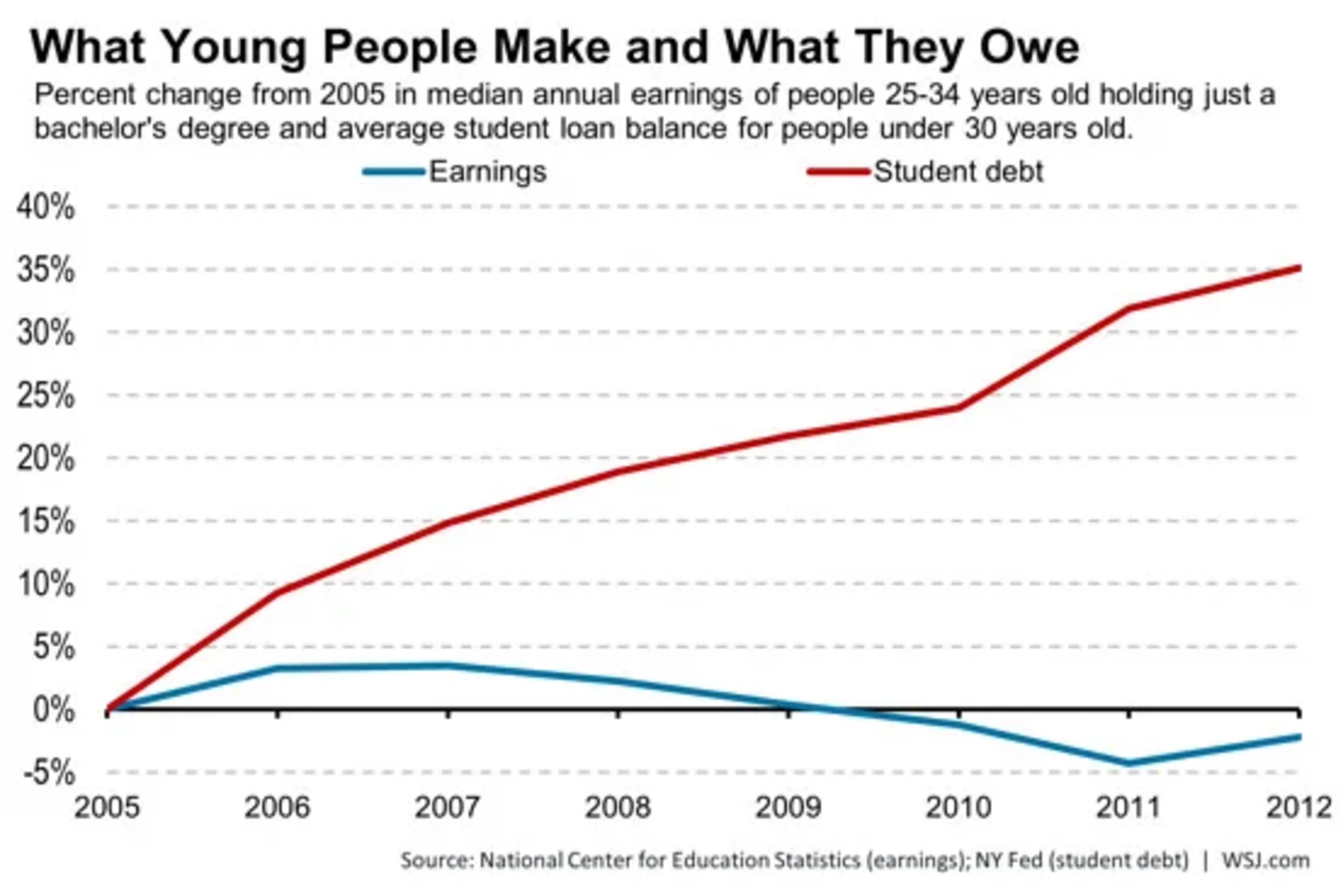

In 2013, Forbes reported more than half of graduates under 25 were unemployed or underemployed, making loan repayment seemingly impossible.3 In fact, in 2014 more than 13% of all student loan borrowers (2.1 million people in total) defaulted on their loans.4

Source: Wall Street Journal

The decision to take out student loans is a big one. Once you graduate, you must repay your debt, a process many young and newly financially independent people struggle with. If you find yourself weighed down with student debt, you need to understand your options. We’ve put together this guide to help you understand what you need to know about student loans, debt, bankruptcy, and your financial future.

Paying for College Without Loans

Before you take out student loans, consider all your options. Depending on your financial situation, you may have a few opportunities to eliminate or minimize your need for loans.

Family Savings: If possible, use family savings and income to pay for at least 30% of your college tuition fees.5 To make this money go further, you may want to consider in-state colleges or living at home instead of in a dorm.

Grants and financial aid: If your family can’t help pay for your tuition, you could qualify for a grant or financial aid. Grants and financial aid, like scholarships, do not have to be paid back. They are awarded based on need and are usually funded by state and federal governments, colleges, and nonprofits. You can apply for several grants at a time, but to qualify for federal grants or financial aid, you need to submit a Free Application for Federal Student Aid (FAFSA).

Scholarships: There’s no risk to applying for as many scholarships as possible. Consider scholarships based on your family background, ethnicity, location, field of study, religion, gender, and extracurricular activities. Look for local organizations like the Rotary Club that award students from your area. There are many scholarship directories like CollegeBoard that can make the search easier.

Crowdfunding: Asking people to help pay for college on sites like GoFundMe is becoming increasingly popular. Crowdfunding sites allow people to donate money to causes and projects they feel are important. Students have run crowdfunding campaigns to help them covering the costs of housing, books, computers, and even tuition. This should be a final resort-- because of the number of crowdfunding campaigns, you shouldn’t rely on your campaign gaining traction.

Understanding Your Loan Options

If you need to take out loans, do plenty of research beforehand. Loans differ by type and lender, and all have their own interest rates and terms of repayment. Be sure you know everything about your loan before taking on debt.

Federal Direct Student Loans: Direct loans, including Federal Stafford Loans, are funded by the US government. They are the most common type of student loan and offer lower interest rates than many other programs. When you graduate, Direct Loans offer various repayment options to suit your current income.

Subsidized: A Subsidized Direct Loan doesn’t require lenders to pay the loan back while they’re at least enrolled in school part-time. Additionally, the government pays interest on the loan while you're in school. Subsidized Direct Loans are usually given to students whose families show financial need and make less than $50,000 a year. After graduation, borrowers can expect interest rates below 6.8%. A student can only receive a total of $23,000 in Subsidized Direct Loans as an undergraduate and $65,000 total as a graduate or medical student. You can only receive Subsidized Direct Loans for 150% of the time duration of your program. That means if you are enrolled in a 4-year bachelor’s degree program, you can receive the Direct Loan for 6 years.6

Unsubsidized: Unlike a Subsidized Direct Loan, with an Unsubsidized Loan you’re responsible for paying all the interest that accumulates while you’re in school. Your payments are still deferred until graduation, but they’ll include 100% of the interest on the loan. All students are eligible to apply for Unsubsidized Direct Loans, regardless of family financial status. Students can borrow $5,500 to $12,500 of Unsubsidized Direct Loan money annually.6

PLUS: PLUS loans are available to parents of dependent college students and to independent graduate students. PLUS loans cover the costs of education not taken care of by other financial aid options. They allow parents to help finance their children’s educational costs. There is no maximum amount for PLUS loans and the interest is fixed at 7.21%. 7

Perkins: Perkins loans are in high demand because of the fixed 5% interest rate. The government further subsidizes the loan by paying the interest while you’re still in school. Perkins loans are reserved for students who show exceptional financial need. The government limits the amount of Perkins funds at each college, but the school chooses which students receive the loans. You can receive $5,500 in Perkins loans each year, for a maximum of $27,500 over 5 years.6

Private: Private loans are generally used when other aid can’t cover your educational costs. They’re given by private lenders like banks and credit unions. Private loans are similar to personal loans, and interest rates are based on credit history and your perceived ability to repay the loan. Because of higher interest rates, private loans can be difficult to pay off. The interest rate can be fixed or variable, and repayment may be required while you’re still in school.8

Student Loan Repayment Programs

According to the US Federal Student Aid website, once you’re out of school or drop below half-time enrollment, you’ll receive a 6-month grace period and then must begin your payments. However, there are some options to make repayment easier, give you more time, or cancel some of your debt.

Deferment

Federal loans offer deferment while you are in school at least part-time. Loan deferment is also available if you are unemployed, underemployed, or experiencing economic hardship (this includes participation in extended community service, like the Peace Corps). Students engaged in active military service as well as those returning from service also qualify.9

Forbearance

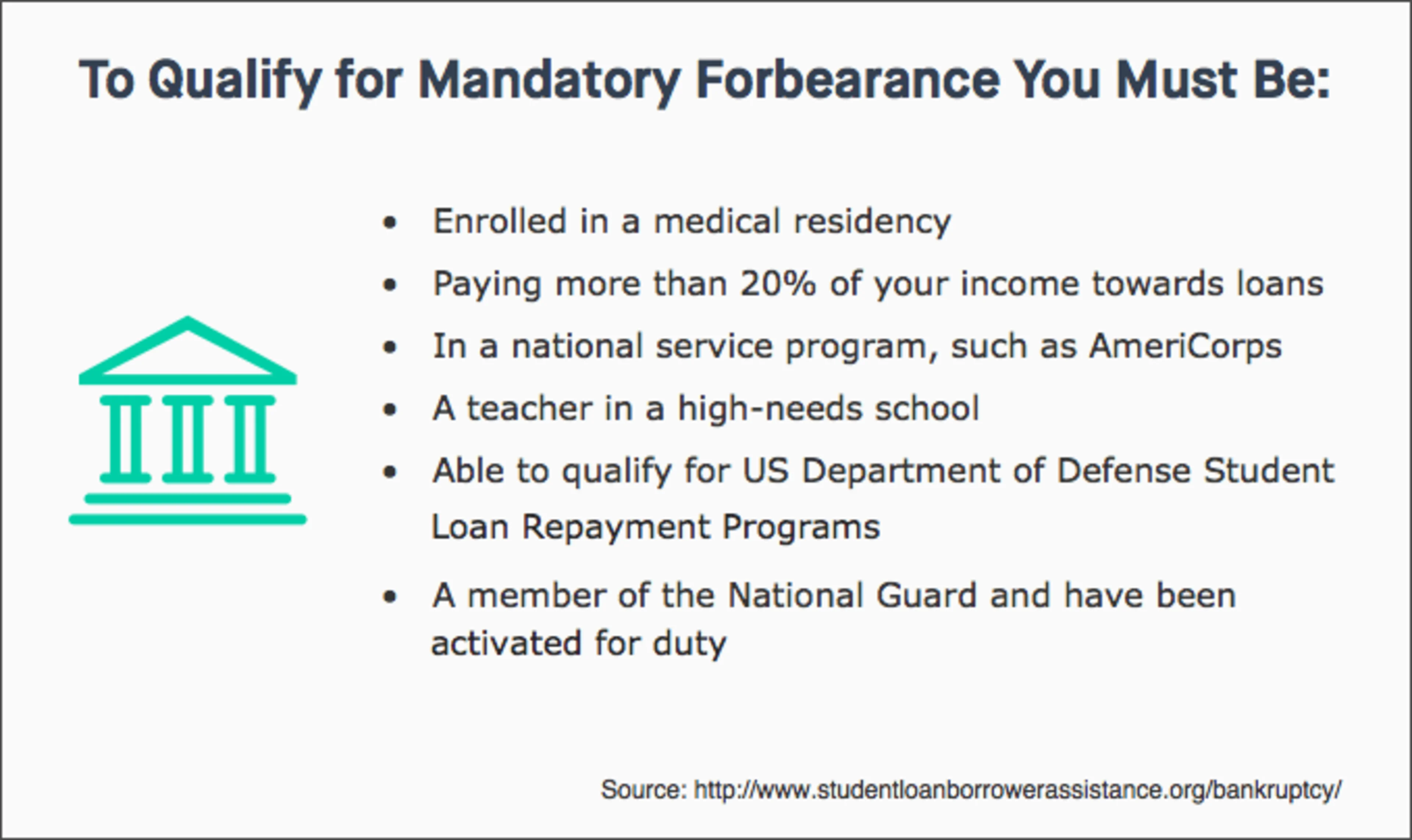

If you can’t make your loan payments and don’t qualify for deferment, discretionary or mandatory forbearance is an option. This lets you reduce or delay loan payments for up to 12 months. With Discretionary forbearance, your loan provider can decide to grant your request to suspend or reduce payments due to financial troubles or medical issues. With mandatory forbearance, the lender is required to grant you leniency on your loan payments.10

Forgiveness

In rare cases, you can void portions of student loan debt, including if you fall into any of the following categories:

Teachers who work for 5 years in low-income elementary or secondary schools can qualify for up to $17,500 of both subsidized and unsubsidized loan forgiveness through the

Under the Public Service Loan Forgiveness Program, borrowers who make 120 payments and work full-time in a public service role can receive forgiveness for the remaining balance of the loan.

People working in education, military service, public libraries, law enforcement, and other service-related professions may qualify.

Perkins Loans may also be forgiven for people who work in service professions, like firefighters, corrections officers, nurses, and Peace Corps volunteers.

Alternative Repayment

Instead of paying an evenly divided sum across the life of your loan, consider a graduated repayment plan. It lets you start with smaller monthly payments and increase over time. This is a great idea for people starting out in an entry-level job who expect to increase their salary as time goes on. You also have options to extend the loan over 25 years, or to pay based on your income.11

Debt Management

Planning how to pay off your student loans can be a daunting task. And as time passes, you may accumulate additional debt in the form of credit cards, auto loans, or mortgages. No matter your situation, managing your debt is an important part of your financial future and personal happiness. Here are some things to consider while creating your debt payoff plan:

Budgeting: Creating and actively managing your monthly budget will help you figure out what loan repayment plan will work best for you. The best way to build a budget is to precisely track all your income and expenses in a month. Then consider additional expenses that come around only once or twice a year, like insurance payments or car registration. Add one-twelfth of those costs to your monthly budget. Many people use spreadsheets to track spending, but if you like to see information in graphs and tables on your computer or mobile device, you could try a free budgeting software program like Mint.

Consolidation: Loan consolidation lets you roll all your Direct Loans into one payment, and may give you the option to extend the loan to as long as 30 years. Consolidating loans usually means you’ll lose any benefits tied to the original loan, such as lower interest rates and the possibility to cancel payments. However, rolling your loans into one payment may help you simplify your budget.

Tax Deductions: The IRS offers tax breaks on student loan interest paid throughout the year. There are certain income requirements to qualify to take the deduction, but if you do qualify, the deduction can be up to $2,500. So come April, make sure you file your loan interest statements.12

Debt Prioritization: Not all debt is equal. Unpaid loans with higher interest rates will cost you more in the long run, so they should be paid off first. Keep in mind that student loans offer much lower interest rates than other debt you may have, including credit card or auto loans. Consider all your interest rates when building a budget, and try to pay off the highest interest loans first.

Financial Advice: Student loan consulting is a relatively new profession, but it’s in high demand. Consultants collaborate with borrowers to create customized plans for repayment. Working an expert in student loan debt, either from your college, a loan officer, or a private consultant, can help you find repayment and budgeting options you didn’t know existed.13

Bankruptcy

For some, student debt becomes an immovable obstacle, and bankruptcy is the only way out of the financial hole. While it’s possible to relieve student loan debt through bankruptcy, it’s rare and a very complicated process.

Federal law prohibits the US government or private lenders from eliminating student loans by both Chapter 7 and Chapter 13 bankruptcy, unless the borrower can prove that repaying the loans causes undue hardship. Also, filing for bankruptcy doesn’t automatically make you eligible to dismiss your student loans. You must actively request loan forgiveness during the bankruptcy hearing and work with a bankruptcy attorney to file an adversary proceeding for student loan forgiveness.

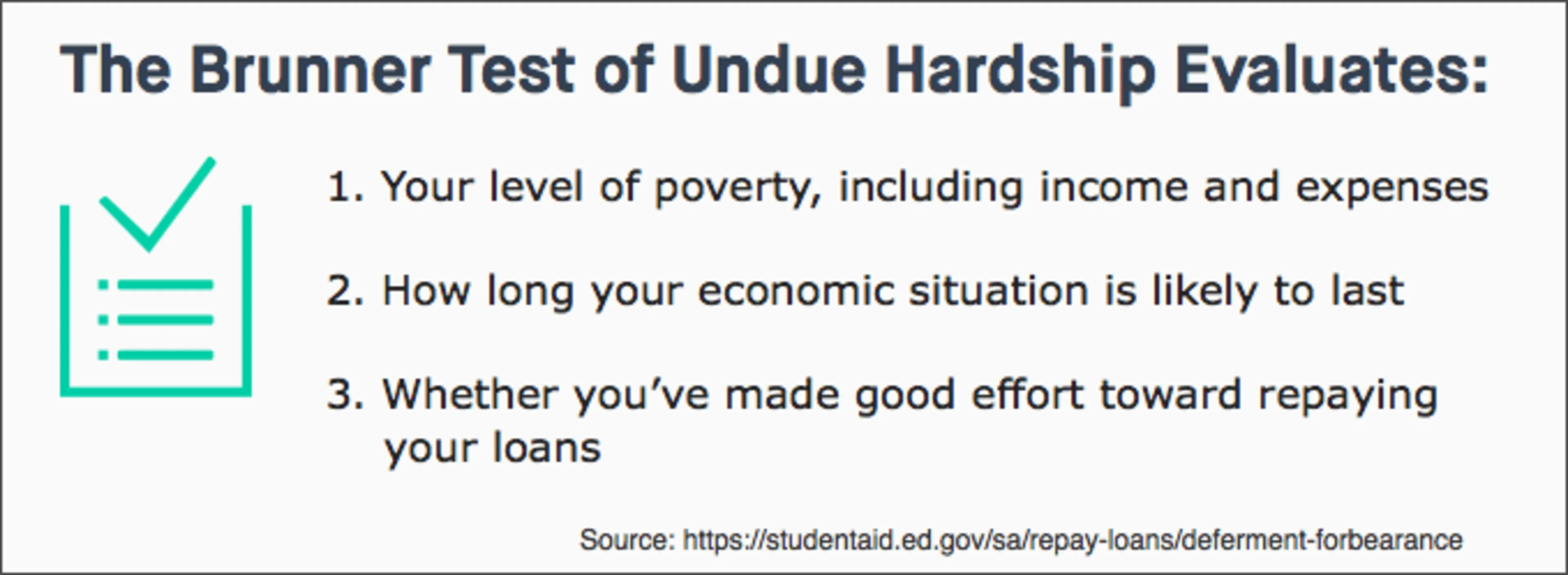

The definition of undue hardship varies by court, so, your chances of clearing student debt via bankruptcy are difficult to gauge. Some courts use the Brunner test to determine if they’ll allow your loans to be discharged.

Brunner test or not, the court will consider many relevant factors in hearing your case, so we recommend you work with a bankruptcy lawyer throughout the process.14

Consequences

There are long-term consequences to filing bankruptcy, so do not take the decision lightly. Bankruptcy stays on your credit history for 7 to 10 years, depending on whether you file Chapter 7 or Chapter 13. This mark on your credit history can impact your ability to open new lines of credit for auto loans, mortgages, and even renting property. Poor credit can also cause problems when applying for some jobs.

Even when you’re drowning in debt, only consider bankruptcy as a last resort. Even though it can potentially wipe away debt, that is the only positive consequence of the decision. The other implications of bankruptcy can impact your financial future for years to come.

Conclusion

If you are struggling with student debt, there are many resources to help. Loan debt can be difficult to deal with, but by understanding the terms of your loans, knowing your repayment options, and sticking to your budget, you can successfully manage your money and continue to reap the benefits of your education.

Lastly, don't be afraid to seek help from the Department of Education, the Federal Student Aid Ombudsman Group, a financial advisor, or a bankruptcy attorney to better understand your personal situation. Your debt isn't an obstacle you have to overcome alone.

Looking to hire a bankruptcy lawyer? Check out our recent award winners to find the best in your area:

Legal Disclaimer: The materials provided in this article are for informational purposes only and not for the purpose of providing legal advice. You should contact an attorney to obtain advice with respect to any particular issue or problem

Amanda RonanAuthor

Amanda Ronan is a contributing author for Expertise.com, and is a Community Editor for Round Table Companies, a creative agency that helps build brand reputation through storytelling. She has over 12 years experience as a teacher in applied language education, and is a graduate of Loyola Marymount University with a Master’s Degree in Education.

Sources

1.https://www.debt.org/students/ 2.http://ticas.org/sites/default/files/pub_files/Debt_Facts_and_Sources.pdf 3.http://www.forbes.com/sites/moneybuilder/2013/02/01/alarming-number-of-student-loans-are-delinquent/ 4.http://thinkprogress.org/education/2014/08/06/3468269/student-loan-defaults-rise/ 5.http://www.washingtonpost.com/blogs/wonkblog/wp/2014/07/31/families-are-finding-alternatives-to-student-loans/ 6.https://studentaid.ed.gov/sa/types/loans/subsidized-unsubsidized 7.https://studentaid.ed.gov/sa/types/loans/plus 8.https://www.salliemae.com/student-loans/ 9.https://studentaid.ed.gov/sa/repay-loans/deferment-forbearance 10.https://studentaid.ed.gov/sa/repay-loans/deferment-forbearance 11.http://www.businessinsider.com/manage-your-student-loan-debt-2013-7 12.http://www.irs.gov/publications/p970/ch04.html 13.http://www.forbes.com/sites/learnvest/2013/07/24/secrets-of-a-student-loan-consultant/ 14.http://www.nolo.com/legal-encyclopedia/student-loan-debt-bankruptcy.html