Pros

- Doesn’t charge lender fees

- Quick pre-approval process

- Lists transparent interest rate information online

Cons

- Not available nationwide

- No FHA, VA, or USDA loans

- No branch locations

Established in 2016, Ally Bank became a top mortgage lender in the industry for its 100% online application that you can complete in 15 minutes or less, no lender fees, and down payments as low as 3%.

Below, we take a closer look at Ally Bank’s home mortgage options, mortgage rate information, and exclusions and limitations to help you determine if Ally is the right lender for you and your family.

We reviewed the best mortgage lenders, and Ally Bank ranked fourth on our list due to its easy-to-navigate 100% online application, no lender fees, and quick closing time frame.

In 2019, Ally announced a partnership with Better Mortgage to create an end-to-end digital experience for borrowers looking to get a mortgage loan with Ally. Better Mortgage handles the processing, underwriting, and closing of loans paired with Ally’s competitive rates and funding. This partnership allows for a simple and easy online application process and quick pre-approval timeline of three minutes or less.

With the company’s customized rate quote tool, shoppers can personalize their quotes without sharing your personal information. The tool also helps explain how discount points could impact your closing costs and interest rates to help you better compare Ally’s rates with other lenders.

One downside to Ally is the company doesn’t offer any government-insured mortgage products FHA, VA, or USDA loans. These loans are often ideal for borrowers with lower credit scores and limited down payment funds.

However, borrowers with less-than-stellar credit can look into the Fannie Mae HomeReady mortgage program offered by Ally. This program allows homebuyers to put down a 3% down payment and requires a debt-to-income (DTI) ratio of no more than 50%, which is higher than the traditional 43% DTI requirement for most loan types.

Ally offers both home loans and mortgage refinancing.

One of the lender’s stand-out offerings is its jumbo loans — a loan that exceeds the conforming mortgage loan limits set by the Federal Housing Finance Agency (FHFA). For 2022, those limits are $647,200 for a single-family home and up to $970,800 for high-cost areas.

Ally offers jumbo loans for up to $4 million and can be used for primary residences, vacation homes, and investment properties. However, Ally’s jumbo loans come with strict requirements.

Borrowers can expect the following jumbo loan requirements:

A minimum credit score of 700

A debt-to-income ratio no higher than 43%

A down payment minimum of 20%

While Ally does offer a variety of common mortgage products, you’ll need to look elsewhere for government-backed loans like FHA, USDA, and VA. These loans are typically geared toward borrowers with low credit scores as they come with less restrictive eligibility requirements.

The lender doesn’t offer speciality loans like construction loans or reverse mortgages, either.

Rather than listing specific interest rate information because it tends to fluctuate on an almost daily basis, we instead evaluated Ally’s mortgage rate transparency.

For a $350,000 home loan for a single-family primary residence with 20% down in Texas, Ally listed a variety of rate estimates for both fixed and adjustable-rate loans.

You can also plug in a few pieces of information (ZIP code, home price, down payment, estimated credit score, property type, and property use) for a customized rate.

If you’re not in a hurry to choose a lender, you can also sign up for Ally’s weekly email that lists the lender’s current rates without needing to refer back to the site.

One of the perks of choosing Ally as your lender is that you get to skip lender fees. Oftentimes, a mortgage comes with the application, origination, processing, or underwriting fees.

According to Value Penguin, average lender fees can amount to $1,387 for a home loan of $198,000. Skipping these fees can keep money in your pocket for any of the unexpected costs that come with homeownership.

However, borrowers should still plan to pay some closing costs, which include appraisal and title service fees. The lender estimates that closing costs can cost between 1% to 2% of the home’s purchase price.

Ally looks at four primary factors to determine a borrower’s mortgage eligibility.

Your debt-to-income ratio: The lender will compare your gross monthly income to the total amount of your monthly debt payments. Your DTI should be below 43%, but keeping this ratio as low as possible will increase your chances of being approved at a competitive rate.

Your credit score: Ally doesn’t specifically list credit score requirements on their website, but it does state that most lenders require a minimum score of 640 for most loans and 700 for jumbo loans.

The down payment you can put down: The lender offers some loan types that require a minimum down payment as low as 3%. However, for a jumbo loan, borrowers need to put down a minimum 20% down payment.

Your employment history: Ally also requires proof of income and that you have a steady income to prove you can afford monthly mortgage payments.

Ally offers a completely digital mortgage application process. In 2019, Ally partnered with Better Mortgage to help streamline its online application. With this partnership, Better Mortgage processes, underwrites, and closes the loan using Ally’s rates and funding.

The company boasts a simple and easy application process that allows borrowers to security upload documents and e-sign disclosures. If you run into any problems during the application process, Ally’s loan officers are available via text or phone.

Once the application is complete, Ally states that pre-approval can happen in as little as three minutes.

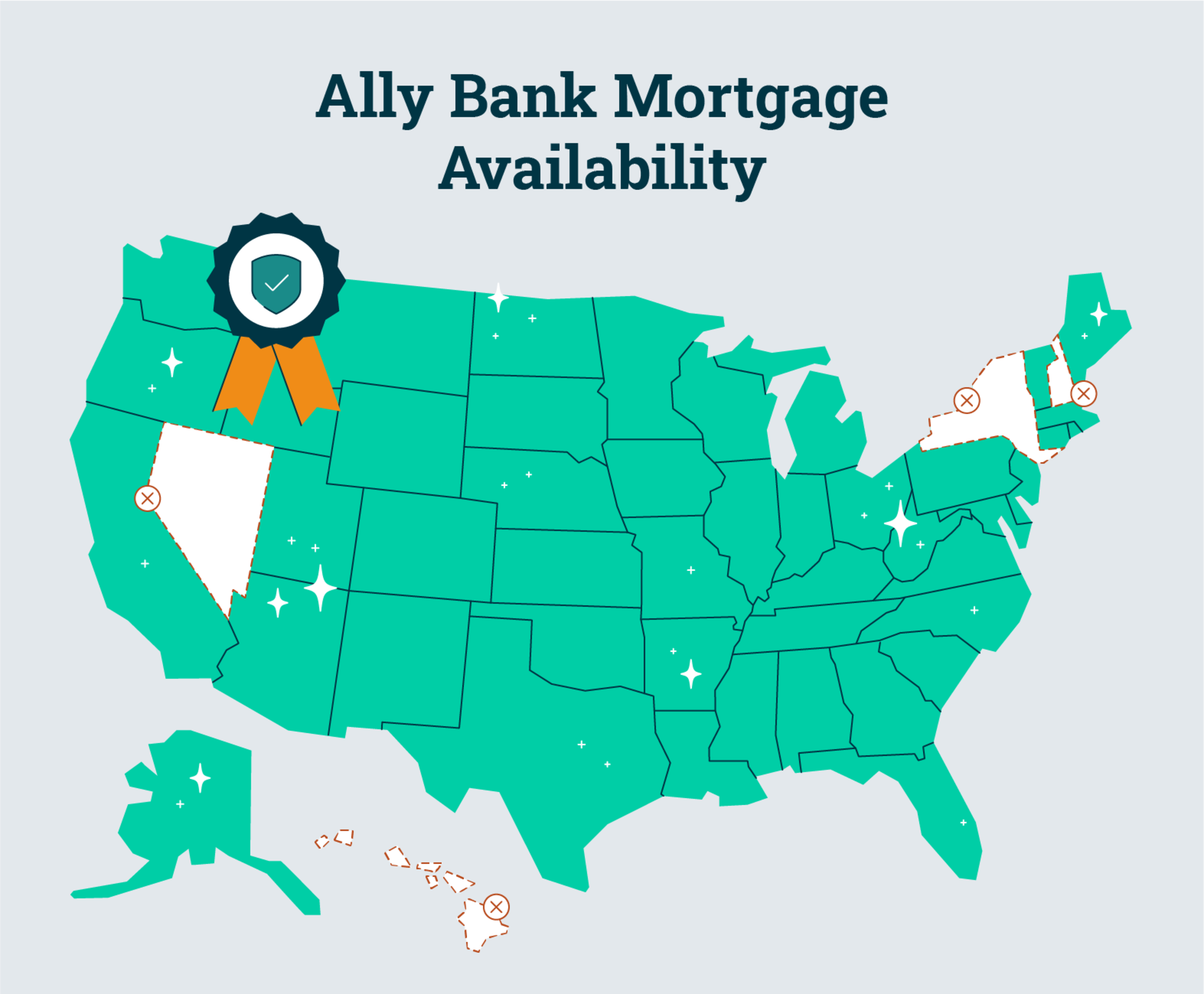

Ally’s mortgages are available to borrowers in 46 states excluding Hawaii, Nevada, New Hampshire, and New York.

Below we compare Ally against some of the industry's top mortgage lenders.

Ally and Better Mortgage are two very similar mortgage lenders. Both are online lenders offering a 100% digital application process. In fact, Ally and Better Mortgage partnered together in 2019 so Ally borrowers could benefit from the Better Mortgage digital platform.

If you’re looking for an FHA loan, Better Mortgage is the clear pick as Ally doesn’t offer this loan type. Ally doesn’t offer mortgages nationwide, so if you’re in a state that Ally doesn’t service, Better Morgage is a good alternative that’s available nationwide.

Ally and Rocket Mortgage both offer online mortgage experiences, perfect for the digital savvy borrower looking for a quick pre-approval timeline.

Unlike Ally, Rocket Mortgage offers two government-backed loan options (VA and FHA mortgages). Rocket Mortgage operates in all 50 states, so if you live in one of the four states that Ally Mortgage doesn’t, Rocket Mortgage may be a good choice for you.

However, Rocket Mortgage charges lender fees for its home loans, which includes origination and application fees. If you’d like to avoid these costs, Ally is the better choice as the company doesn’t charge any application, origination, processing, or underwriting fees.

Ally receives a mixture of positive and negative reviews on the Better Business Bureau and Trustpilot websites. The company receives an A rating from the BBB and a Trustpilot score of 1.6 out of 5.

It should be noted that the majority of the reviews on BBB and Trustpilot are about the Bank’s other offerings such as car loans and checking accounts rather than mortgages specifically.

For mortgage-specific reviews, we turned to Zillow. Ally received a 4.4 out of 5 score from Zillow, which lists over 300 reviews about the lender’s home loan process.

Below is a snapshot of a few recent Ally reviews posted to Zillow.

“I'm so happy! Where do I start? The journey to home ownership has finally come to fruition for me. I have had the absolute best experience using Ally Bank. The entire team I worked with from Juan, Destiny, Julie, and Markeith were incredible. The team informs you of every step, provides support when you have questions and the experience is seamless. I absolutely loved the digital experience because I was able to upload, sign, and download documents right away. The communication has always been above and beyond. In my search, I have scrolled through reviews trying to make a decision on what company to choose and I am thankful for the reviews that led me to Ally Bank. Ally Bank has been a dream to work with and I will forever recommend them to friends and family.” — Caris S. from Trenton, New Jersey, 8/25/2022

“We went with Ally after shopping around having used them for our banking already. Their mortgage application process and interface is amazing. When shopping for a house, we were able to independently update our preapproval letter on the fly (up to the amount we had been approved for), which was super handy when looking and our plans changed. Then with all you have to fill out and attach throughout the mortgage process, the app made it super easy and clear. The people we worked with were friendly and responsive. Rates and closing costs/fees couldn’t be beat by 3-4 others.” — rswa246322 from St. Louis, Missouri, 5/30/2022

“This was the second time I used Ally Mortgage. The first was last year, and everything was wonderful. I used them again this year for a condo in Tampa FL. What a nightmare. The in-person closing took 5 hours because the title company and Ally couldn't communicate in advance apparently. The title company was treating it as a second home and Ally was treating it as an investment property. Neither company bothered to communicate with me, the borrower. We ended up doing the signing three times before they got all the docs correct. To make matters worse, why on earth would Ally assign a closing specialist based on the west coast when every other aspect of this transaction was east coast based (where I live, where the new property is located, etc.)[?] My closing specialist was next to useless because he didn't clock in until noon eastern time every day. I will never use Ally again.” — Lou from Thonotosassa, Florida, 8/5/2021

“We closed in 29 days. Neither our realtor nor selling agent thought it possible with a bank for a lender but we were extremely on top of submitting all of the necessary paperwork, disclosures, etc. and they processed it FAST. Emily, Patrick, Julie, & Tammy were amazing and always on point with communication by phone AND email, and we had a lot of questions as [first-time] home buyers. Special shoutout to Tammy who wasn't even our expert but filled in while our closing expert was out and helped calm us down at the final hour. We had a great realtor with a strong network, and Ally helped us seal the deal. Our sellers had a FIRM closing date of 30 days or less so we were extremely concerned about them backing out if we couldn't meet that deadline, but Ally assured us they could do 30 days, so we went with them and we're just happy everything went smoothly and worked out in our favor.” — S C from Palmetto, Florida, 1/4/2022

Below, we answer some of the most common questions about Ally’s home mortgages.

So, who is an Ally loan good for?

One of Ally’s top perks is its 100% online application process, so for a borrower that appreciates the ease of being able to upload documents and sign disclosures online, Ally is a top lender choice.

Ally is also a good option for those that are looking to save on lender fees, as the company doesn’t require application, origination, processing, or underwriting fees.

The biggest downside to Ally is its lack of government-backed loan options, which come with less restrictive borrower requirements. If you have a low credit score, we recommend comparing lenders like Guaranteed Rate or PennyMac that offer government-backed loans like an FHA, VA, or USDA, as they can be more attainable for borrowers with low credit.

Beginning with a list of 22 mortgage lenders, we evaluated each company based on a variety of criteria, including:

Customer satisfaction rankings: We scored companies based on their rankings from the Better Business Bureau, Trustpilot, and the 2022 J.D. Power U.S. Mortgage Origination Satisfaction Study.

Mortgage rate transparency: Companies that clearly list sample interest rates for a variety of loan types on their website scored higher in this category compared to lenders that do not advertise rates. We also awarded points to companies that made it easy to get an online customized quote without divulging personal information.

Loan fees and costs: We scored companies higher that are transparent about their loan fees and costs associated with their mortgages.

Minimum down payment and credit score requirements: We compared each company's minimum down payment and credit score requirements for a conventional loan.

Ease of application: We rated each company on how easy it is to apply for a loan. Companies that offer a fully digital experience scored the highest.

State availability: Lenders that operate nationwide scored the highest in this category.

Loan types offered: We awarded points to companies that offer the most common loan types, with companies offering more loan types scoring higher in this category.

While interest rates are certainly an important factor when choosing a mortgage lender, we did not account for the currently available rates within our methodology section. This is because rates fluctuate often and your exact rate will depend on your location, credit score, and credit report.

Because of this, we instead reviewed companies based on whether they provide transparent interest rate information on their site and whether you can get a custom quote online.

Expertise.com StaffAuthor

Step into the world of Expertise.com, your go-to hub for credible insights. We don't take accuracy lightly around here. Our squad of expert reviewers, each a maestro in their field, has given the green light to every single article you'll find. From rigorous fact-checking to meticulous evaluations of service providers, we've got it all covered. So feel free to dive in and explore. The information you'll uncover has been stamped with the seal of approval by our top-notch experts.

![6 Best Pest Control Companies [2023] Hero Image](https://images.ctfassets.net/k00sbju4hbzq/1WQPzQPrrXLyuRrZSHYNan/6a19175944a2bbaa190852cd00830d7e/Artboard_4.png?fit=fill&w=384&q=75)